Overview

Syria's energy sector is in turmoil because of the ongoing hostilities between government and opposition forces. Syria's oil and natural gas production has declined dramatically since March 2011 because of the conflict and because of the subsequent imposition of sanctions by the United States and European Union in particular. Syria's energy sector is unlikely to recover in the near term.

Since the onset of protests in March 2011, Syria's energy sector has encountered a number of challenges. Damage to energy infrastructure—including oil and natural gas pipelines and electricity transmission networks—and the effects of Western-led sanctions have combined to hinder the exploration, development, production, and transport of the country's energy resources. While Syria is not a major player in the global energy system, the ongoing conflict will continue to have consequences in domestic and regional energy markets.

Syria, previously the eastern Mediterranean's leading oil and natural gas producer, has seen its production fall to just a fraction of pre-conflict levels. Syria is no longer able to export oil, and as a result, government revenues from the energy sector have fallen significantly. Prior to the current conflict, Syria's oil sector accounted for approximately one fourth of government revenues.

As of January 2014, Syrian officials reported the overall economic losses from the conflict reached more than $20 billion. Of that total, estimates from mid-2013 indicate that the losses from the hydrocarbons sector have topped $12 billion, from both direct causes (damage to infrastructure, spillage, and theft) and indirect causes (lost exports). According to the Syrian government, damage to the country's energy infrastructure and spilled or stolen oil and natural gas cost the country approximately $1 billion through the end of July 2013. The loss of Syria's oil exports, limited by sanctions by the United States, European Union (EU), and others, accounted for much of the remaining economic losses. In April 2013, the EU agreed to allow oil imports from Syria, although only from opposition groups, which do not currently have access to Syria's oil export infrastructure. In June 2013, the EU extended all sanctions on the Syrian government's oil exports for an additional 12 months.

Syria faces major challenges in supplying heating and fuel oil to its citizens, and electricity service in much of the country is sporadic as a result of fighting between government and opposition forces. Further, the exploration and development of the country's oil and natural gas fields is delayed indefinitely in most places, although the Syrian government did reach an exploration agreement with a Russian company in late 2013. Nevertheless, even when the fighting subsides, it will take months, or possibly years, for the Syrian domestic energy system to return to pre-conflict operating status.

| Oil (million barrels) | |||

| Proved reserves, 2014 (million barrels) | Total oil supply, 2012 (thousand bbl/d) | Total petroleum consumption, 2012 (thousand bbl/d) | Reserves-to-production ratio |

| 2,500 | 71 | 258 | 43 |

| Natural gas (billion cubic feet) | |||

| Proved reserves, 2013 | Dry natural gas production, 2012 | Dry natural gas consumption, 2012 | Reserves-to-production ratio |

| 8,500 | 228 | 228 | 26 |

| Electricity | |||

| Generating capacity, 2011 (gigawatts) | Electricity generation, 2011 (billion kilowatthours) | Electricity consumption, 2010 (billion kilowatthours) | Distribution losses, 2010 (billion kilowatthours) |

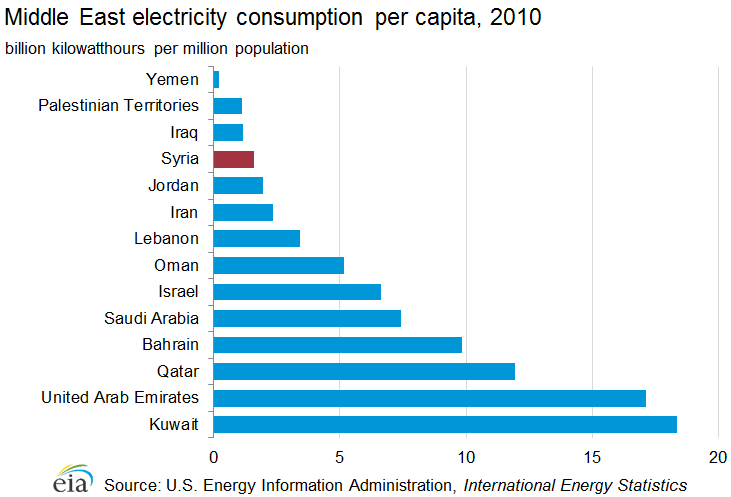

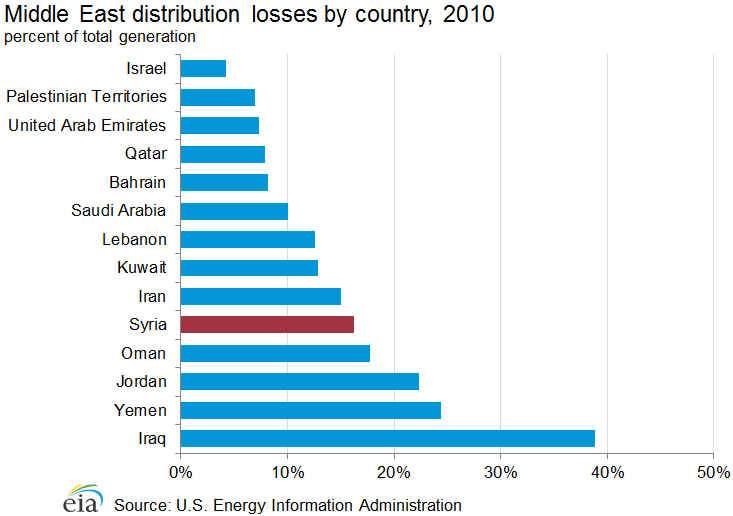

| 7.8 | 43.8 | 35.6 | 7.1 |

| Source: U.S. Energy Information Administration, International Energy Statistics and Short-Term Energy Outlook, Oil & Gas Journal | |||

Sector organization

In 1964, Syria passed legislation that limited licenses for exploration and investment to the Syrian government. The Ministry of Petroleum and Mineral Resources oversees the Syrian oil and natural gas sectors, and is in charge of setting policy priorities and coordinating the efforts of the state-led companies that operate in the sector. Given the turmoil in Syria since March 2011, the following information largely reflects the pre-conflict operating status of Syria's oil and natural gas sector.

The General Petroleum Company (GPC) oversees the strategies for exploration, development, and investment in Syria's oil and gas sector, and supervises the activities of its numerous affiliated companies, including the Syrian Petroleum Company (SPC) and the Syrian Gas Company (SGC). The SPC is Syria's largest state-owned oil company, and it has a number of production-sharing agreements (PSAs) in place throughout the oil sector. Most of the country's PSAs are split equally between the SPC and its partners. These arrangements often ensure that the Syrian government retains a certain percentage of the oil produced in its fields as royalties. Contracts regularly last up to 25 years.

The SPC operates through several subsidiaries, the most notable being the Al-Furat Petroleum Company (AFPC), which is a joint venture between the SPC, Royal Dutch Shell, the Chinese National Petroleum Company (CNPC), and India's Oil and Natural Gas Corporation (ONGC). Other SPC subsidiaries include the Deir Ez-zor Petroleum Company, the Syria-Sino Alkawkab Oil Company, the Hayan Petroleum Company, the Oudeh Petroleum Company, and the Dijla Petroleum Company. International oil companies with interests in Syria prior to the conflict included Gulfsands, Sinopec, and Total, as well as several other smaller companies. By most accounts, nearly all of Syria's foreign partners have left the country.

The General Organization for Refining and Distribution of Petroleum Products (GORDPP) manages the country's downstream portfolio for both oil and natural gas, and it oversees the operations of the Banias Refinery Company and the Homs Refinery Company, among other duties. Other important state entities overseen by the GORDPP include the Syrian Company for Oil Transport (SCOT, which operates the country's pipelines), Mahrukat (which deals with refined products), and Sytrol (which is the state marketer of petroleum products).

The Syrian Gas Company (SGC)—which falls under the GPC—is the key entity in Syria's upstream natural gas operations, a position it inherited after being split off from the SPC in 2003. Syria's natural gas distribution network is managed by the SCOT. The majority of Syria's gas-processing plants are operated by state—owned firms—led by the SPC—but there are a handful that are operated by international companies.

The Ministry of Electricity oversees the electricity sector in Syria, while the General Establishment for Electricity Transmission operates the country's transmission system. Syria also has separate entities for the generation and distribution of electricity.

Petroleum and other liquids

Syria's oil sector has been in a state of disarray since 2011. Production and exports of crude oil have fallen to nearly zero, and the country is facing supply shortages for some refined products.

The Oil & Gas Journal estimated Syria's proved reserves of oil at 2.5 billion barrels as of January 1, 2014, a total larger than all of Syria's neighbors except for Iraq. Much of Syria's crude oil is heavy (low gravity) and sour (high sulfur content), making the processing and refining of Syrian crudes difficult and expensive. Further, because of sanctions placed on Syria by the European Union in particular—which accounted for the vast majority of Syrian oil exports previously—there are a limited number of markets available that can import and process the heavier Syrian crudes. As such, the loss of oil export capabilities has severely limited Syrian government revenues, particularly the lost access to European markets, which in 2011 imported $3.6 billion worth of oil from Syria, according to news reports.

Syrian oil production is at a virtual standstill, and the lack of crude oil has led to the country's refineries operating at lower than normal capacities. This resulted in supply shortages for some refined products. Further, sanctions—and the resulting loss of oil export revenues—make importing petroleum products difficult. Oil theft is also a problem, with Syrian officials claiming that hundreds, possibly thousands, of barrels of crude oil are being stolen and shipped to neighboring countries each day.

Exploration and production

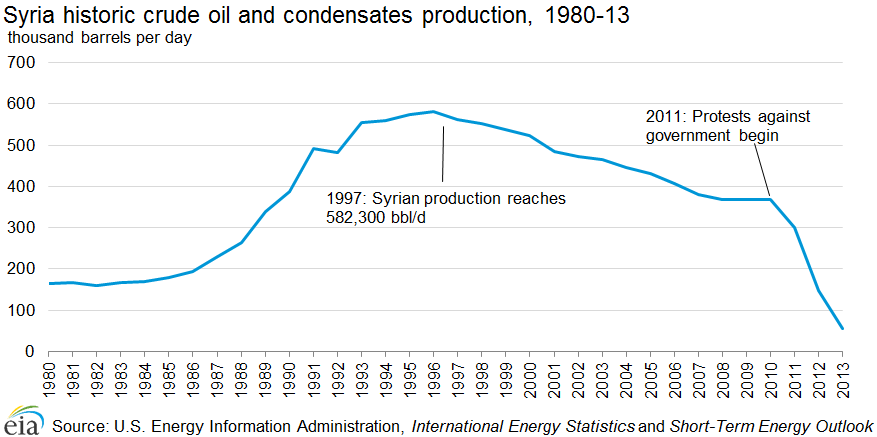

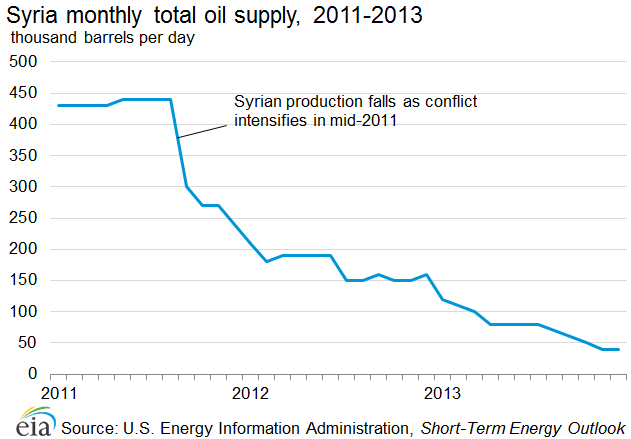

Syria's oil production, which averaged over 400,000 barrels per day (bbl/d) between 2008 and 2010, was less than 25,000 bbl/d in January 2014.

With the onset of sanctions by the United States, European Union, and others, many of the international oil companies (IOCs) and national oil companies (NOCs) doing business in Syria ceased operations, significantly limiting Syria's exploration and production capabilities. The managing director of the GPC claimed that heavy oil production in Syria stopped in early 2013 and that the rest of the country's production was down to 15,000 barrels per day (bbl/d) or less. Most of Syria's existing oil fields are located in the east near the border with Iraq or in the center of the country east of the city of Homs. According to news reports in late 2013, the Syrian government has lost control of nearly all of the country's major oil fields.

Most of the IOCs previously involved in Syria's energy sector have suspended operations, and according to Syrian government officials, the only oil companies still operating in Syria as of September 2013 were Hayan Petroleum and the Elba Petroleum Company, but they are operating without their IOC partners. However, in December 2013 the Syrian government and Russian company SoyuzNefteGaz came to terms on a 25-year exploration agreement in Block 2 offshore.

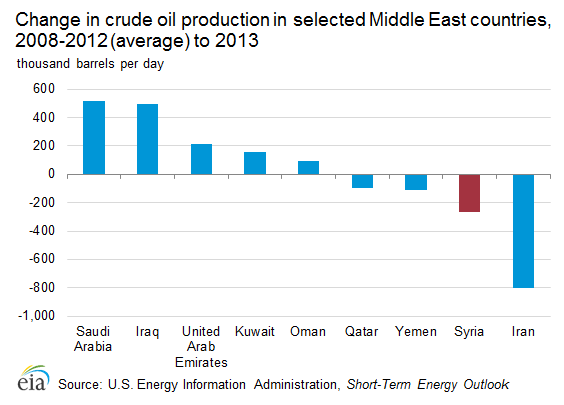

Syria's average oil production from 2008-10 was stable at approximately 400,000 bbl/d, but since the combined disruptions of military conflict and economic sanctions began, the country's production dropped dramatically. The latest EIA estimates indicate that Syrian crude and condensates production has fallen to barely 25,000 bbl/d—including production outside the control of the Syrian government—or a drop of roughly 90% since March 2011 when the conflict began.

Syria's oil fields remain relatively unaffected in terms of damage from fighting and sabotage, but limited opportunities to export crude and other liquids, and limited domestic refining capacity, have resulted in shut-in production. Prolonged shut-ins can reduce the effective capacity of some fields, and the U.S. Energy Information Administration (EIA) estimates that Syria's production capacityâ?�the level of production that could return within one yearâ?�has fallen by nearly 100,000 bbl/d since the start of the conflict.

The years prior to the onset of hostilities saw an increased emphasis on the use of enhanced oil recovery (EOR) techniques in Syria, with several companies promising increased investment in the country's mature oil fields. The AFPC utilized water- and gas-injection systems to aid recovery in many of its fields, and—with little in the way of new discoveries expected—EOR techniques are likely to become increasingly important for ensuring stable output once production returns.

Syria also has shale oil resources, with estimates of reserves ranging as high as 50 billion tons as of late 2010 according to Syrian government sources. The Syrian government delayed a bidding round for the country's shale resources—scheduled for November 2011—because of the political situation in the country.

Imports and exports

Syria's crude oil exports have declined significantly since 2011, and the country is having difficulties importing refined petroleum products.

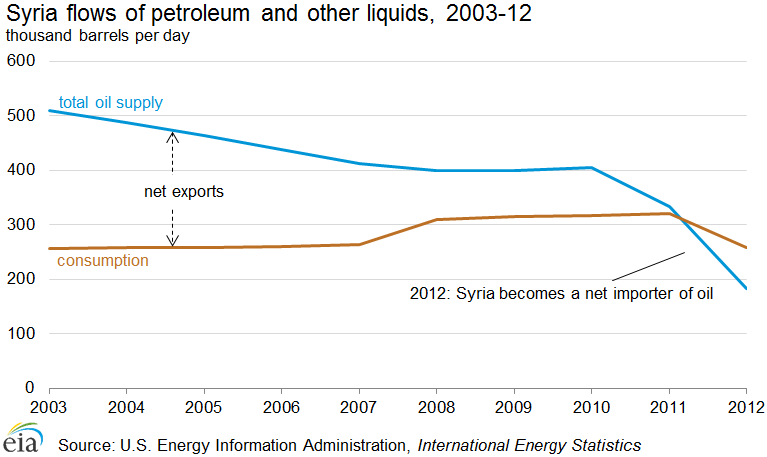

In the years leading up to 2011, Syria began importing more refined petroleum products to meet rising domestic demand. In 2010, the country imported an average of 105,000 bbl/d of refined petroleum products, while exporting just 36,000 bbl/d. At the time, Syria was also exporting over 150,000 bbl/d of crude oil, but the country's crude exports are now effectively zero. In the 12 months prior to March 2011, approximately 99% of Syria's crude exports went to Europe (including Turkey) according to trade data available to EIA.

The ongoing conflict has reduced Syria's production and possibly its refining capacity. Heating oil and diesel fuel are two of the products in short supply. Iraq agreed to send up to 720,000 tons of fuel oil to Syria as part of a one-year supply contract signed in June 2012, and Iran agreed in early 2012 to supply Syria with 900,000 tons per year (approximately 10.4 million barrels per year) of liquefied petroleum gas (LPG). Both of these arrangements help close the supply gap created by the sanctions, but even with lowered demand in Syria, shortfalls are likely to persist.

In May 2013, Iran opened a $3 billion credit line with Syria to help finance the import of crude oil and refined petroleum products. In 2013, Iran sent an average of at least 30,000 bbl/d of crude oil based on trade data available to EIA. Syrian officials estimate the country's import bill for crude oil and refined products was averaging $400 million per month at the end of 2013.

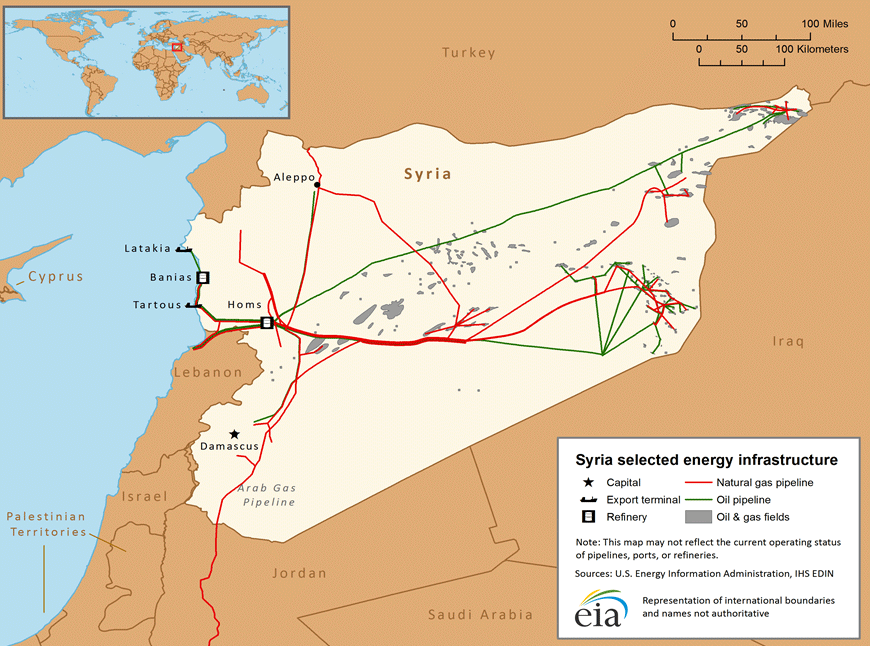

Syria has three export terminals on the Mediterranean Sea, all operated by the Syrian Company for Oil Transport (SCOT) under the GORDPP. Syria has two crude oil export blends, Syrian Light and Syrian Heavy (also known as Souedieh). Since the sanctions on Syria's oil sector came into full effect, total exports have fallen significantly, and they are unlikely to rebound until there is a cessation of hostilities in the country.

Refining and consumption

As of January 2014, Syria's refineries are running at less than full capacity. According to government sources, the combined capacity of Syria's two refineries has fallen to roughly half their pre-conflict output.

Syria has two state-owned refineries, one in Homs and the other in Banias. The combined nameplate capacity of the two refineries at the end of 2013 was just below 240,000 bbl/d according to the Oil & Gas Journal; a total capacity that met only three-fourths of Syria's pre-conflict demand for refined products. With damage to pipelines and other infrastructure around the refinery at Homs in particular, Syrian officials claim that the country's actual refining capacity now sits closer to 50% of its pre-war nameplate capacity. Several proposed refineries are now on hold or cancelled altogether, such as the proposed 100,000 bbl/d facility at Abu Khashab backed by the CNPC, which was cancelled because of the security situation in the country.

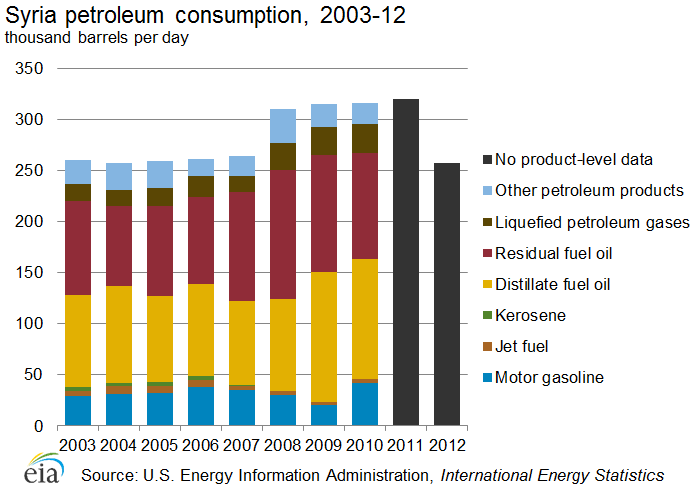

In 2012, Syria's consumption of refined products fell below 260,000 bbl/d, and EIA estimates that 2013 consumption will be even lower once the data become available. The Syrian government continues to subsidize domestic consumption of refined petroleum products. In the first half of 2013 the government spent more than $1 billion on petroleum subsidies, according to the Minister of Petroleum and Mineral Resources.

Natural gas

Syria's natural gas sector has not been impacted quite as severely by the ongoing conflict as its oil sector, although dry production is down by at least 30% compared to pre-conflict totals.

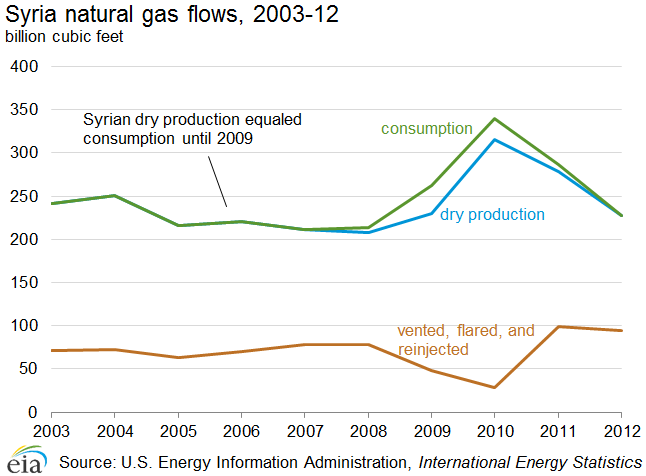

The Oil & Gas Journal reported that Syria held proved reserves of 8.5 trillion cubic feet (Tcf) of natural gas as of January 2014. Like the country's oil fields, the majority of Syria's natural gas fields are in the central and eastern parts of the country. Most of Syria's natural gas is used by commercial and residential customers and in power generation, but Syria also uses its natural gas in oil-recovery efforts, with an average of just over 19% of daily gross production reinjected into the country's oil fields between 2003 and 2012. Syria reduced its venting and flaring of natural gas noticeably over the past decade, with an average of just 2.5% of the country's gross production lost in that way between 2003 and 2012. By comparison, in the 1990's Syria vented or flared roughly 10% of the natural gas it produced.

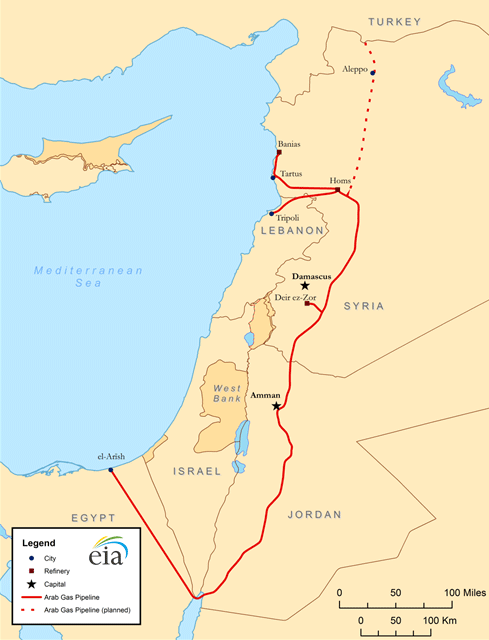

In 2008, Syria became a net importer of natural gas, but the country's current state of conflictâ?�and the attendant sanctionsâ?�could impact the ability of Syria to receive volumes moving forward. The only source of natural gas imports previously, the Arab Gas Pipeline, became the target of attacks as the conflict intensified, forcing the pipeline to shut down as a result. Syria's plans to convert all existing thermal power generation facilities to natural gas-fired plants (many are currently using refined petroleum products) hinge on these volumes being available, but this goal appears out of reach at least in the short term.

| Operator | Facility | Estimated Capacity (MMcf/d) |

|---|---|---|

| SPC | Deir Ez-Zor | 441 |

| Palmyra | 264 | |

| Palmyra (South Middle Area Gas Project) | 247 | |

| Jbessa Plant | 105 | |

| Suweidiya/Hasakah | 23.2 | |

| AFPC | Omar Gas Plant | 230 |

| Suncor | Ebla | 88 |

| INA Naftaplin | Jihar | 141 |

| Stroytransgaz | Palmyra (North Middle Area Gas Project) | 106 |

| Source: IHS EDIN, IHS Global Insight, Trade press, EIA estimates | ||

Exploration and production

Syria's dry natural gas production fell to less than 200 billion cubic feet (Bcf) in 2013 according to estimates from the U.S. Energy Information Administration (EIA).

In 2010, the last year under normal operating conditions, Syria produced 316 billion cubic feet (Bcf) of dry natural gas. By 2012, that figure dropped by 28% to just over 227 Bcf, and EIA estimates that production in 2013 was below 200 Bcf. Prior to the current conflict, more than half of Syria's natural gas production came from non-associated fields, with those volumes being redirected to oil fields and domestic demand centers through the country's domestic pipeline network. In 2012, 25% of Syrian natural gas production was re-injected into the country's oil fields to aid in recovery, a slight increase from the 2002-11 average of nearly 19%. According to Syrian government officials, in 2013 over 90% of the country's natural gas production went to the electricity sector.

Exploration for natural gas in Syria is at a virtual standstill, although the recent agreement between the Syrian government and SoyuzNefteGaz on exploration in Block 2, in Syria's offshore territory, could result in new exploration in the next few years.

Imports and exports

According to press reports, Syria is not currently importing natural gas from Egypt via the Arab Gas Pipeline.

Syria does not currently possess the ability to export liquefied natural gas (LNG), nor are current production levels sufficient to justify exporting natural gas volumes via pipeline. Previously, Syria imported a small amount of natural gas from Egypt to supplement its own domestic production, but volumes dropped by more than 60% between 2010 and 2011 (from 24.4 Bcf to 8.8 Bcf according to Cedigaz data) and ceased altogether in 2012. Those imports came via the Arab Gas Pipeline, which started operating in 2008 and sends Egyptian gas into Syria (near Homs) via Jordan. There were plans to expand the pipeline into Turkey, Lebanon, and eventually Europe, but developments are unlikely in the near term.

U.S. Energy Information Administration, IHS

Representation of international boundaries is not

necessarily authoritative

Electricity

Syria's electricity infrastructure, including power plants, substations, and transmission lines, was an increasingly common target of sabotage in 2013.

In 2010, Syria generated almost 44 billion kilowatthours of electricity, 94% of which came from conventional thermal power plants. The remaining 6% came from hydroelectric power plants. Refined petroleum products and natural gas fuel Syria's thermal generating facilities. Syria plans to convert all thermal generation facilities to run on natural gas as soon as possible, although probably not until after the end of hostilities. Syria's lack of domestic refining capacity, the ongoing sanctions on the country's energy sector and declining natural gas production combine to limit the availability of the necessary fuel for Syria's electric plants, and have contributed to blackouts in many parts of the country.

By early 2013, more than 30 of Syria's power stations were inactive, and at least 40% of the country's high voltage lines had been attacked, according to Syria's Minister of Electricity. Syria's electricity generating capacity was 7.8 gigawatts in 2011, although damage to electricity generating facilities, high voltage power lines, and other infrastructure has likely reduced the country's effective capacity. Distribution losses, already 16% of total generation in 2010, have likely climbed even further.

Prior to the current conflict, the Syrian government hoped to emphasize the importance of renewable energy and laid out plans to develop renewable energy sources in the country. The 11th Five-Year Plan for 2011-2015 made that goal clear, but progress will be slow until the situation in the country stabilizes. Nevertheless, the Syrian Arab News Agency (SANA) reported that a wind project led by a Russian firm began in late 2013, although details on the project are scarce.

Syria, along with Egypt, Iraq, Jordan, Libya, Lebanon, the Palestinian Territories, and Turkey, is a member of the Eight Country Interconnection Project, but the recent developments in Syria's electricity sector leave the future of the project—at least within Syria—in doubt. In 2012, Syria reduced its imports of electricity from neighboring Egypt, Jordan, and Turkey, opting to pursue an arrangement with Iran instead. That agreement would connect 250 megawatts of transmission capacity from Iran to Syria, and came on the heels of the announcement that Syria had suspended purchasing electricity from Turkey. Iran agreed to provide Syria with a $1 billion credit facility in mid-2013, with half of the total earmarked for electric power projects.

In September 2012, Syria's Minister of Electricity announced plans to boost generating capacity by an additional 1.5 gigawatts over the next several years, but like most projects in the country, the current lack of access to international capital makes such an undertaking difficult. Syrian officials announced that the schedule for the construction of 1 gigawatt in new generating capacity (from four new 250 megawatt power plants) would be delayed until the end of 2012, and as of January 2014 there has been no reported progress.

Notes

- Data presented in the text are the most recent available as of February 18, 2014

- Data are EIA estimates unless otherwise noted.

Sources

Agence France Presse

Al-Furat Petroleum Co.

APS Review Oil and Gas Market Trends

The Arab Fund

Arab Oil & Gas Journal

BBC World Wide Monitoring

Business Middle East

The Center for Strategic and International Studies

Daily News Egypt

The Economist

Energy Intelligence Group

European Commission

Financial Times

Government of Syria, Ministry of Petroleum and Natural Resources

Gulfsands Petroleum Co.

IHS CERA

IHS Global Insight

International Energy Agency

International Monetary Fund

Middle East Economic Survey (MEES)

NewsBase

Oil & Gas Journal

Oxford Business Group

PFC Energy

Reuters

Syrian Arab News Agency (SANA)

Syrian News Digest

Syrian Petroleum Company (SPC)

TendersInfo

Transparency International

United Press International

U.S. Energy Information Administration (EIA)

The World Bank